Bayesian state space estimation in Python via Metropolis-Hastings(Open on Google Colab | View / download notebook | Report a problem)

Note: This page was updated on October 26, 2016 to reflect changes in Statsmodels.

Table of Contents

State space estimation in Python via Metropolis-Hastings

This post demonstrates how to use the (http://www.statsmodels.org/) tsa.statespace package along with the PyMC to very simply estimate the parameters of a state space model via the Metropolis-Hastings algorithm (a Bayesian posterior simulation technique).

Although the technique is general to any state space model available in Statsmodels and also to any custom state space model, the provided example is in terms of the local level model and the equivalent ARIMA(0,1,1) model.

%matplotlib inline

import numpy as np

import pandas as pd

import pymc as mc

from scipy import signal

import statsmodels.api as sm

import matplotlib.pyplot as plt

import seaborn as sn

np.set_printoptions(precision=4, suppress=True, linewidth=120)

Suppose we have a time series $Y_T \equiv { y_t }_{t=0}^T$ which we model as local level process:

\[\begin{align} y_t & = \mu_t + \varepsilon_t, \qquad \varepsilon_t \sim N(0, \sigma_\varepsilon^2) \\ \mu_{t+1} & = \mu_t + \eta_t, \qquad \eta_t \sim N(0, \sigma_\eta^2) \\ \end{align}\]In this model, there are two unknown parameters, which we will collected in a vector $\psi$, so that: $\psi = (\sigma_\varepsilon^2, \sigma_\eta^2)$; let’s set their true values as follows (denoted with the subscript 0):

\[\psi_0 = (\sigma_{\varepsilon,0}^2, \sigma_{\eta,0}^2) = (3, 10)\]Finally, we also must specify the prior $\mu_0 \sim N(m_0, P_0)$ to initialize the Kalman filter.

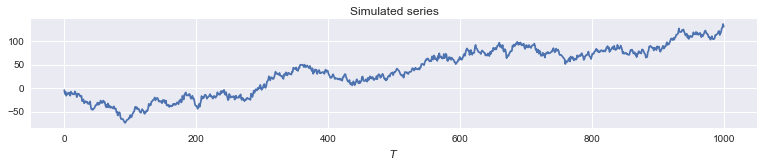

Set $T = 1000$.

# True values

T = 1000

sigma2_eps0 = 3

sigma2_eta0 = 10

# Simulate data

np.random.seed(1234)

eps = np.random.normal(scale=sigma2_eps0**0.5, size=T)

eta = np.random.normal(scale=sigma2_eta0**0.5, size=T)

mu = np.cumsum(eta)

y = mu + eps

# Plot the time series

fig, ax = plt.subplots(figsize=(13,2))

ax.plot(y);

ax.set(xlabel='$T$', title='Simulated series');

It turns out it will be convenient to write the model in terms of the precision of $\varepsilon$, defined to be $h^{-1} \equiv \sigma_\varepsilon^2$, and the ratio of the variances: $q \equiv \sigma_\eta^2 / \sigma_\varepsilon^2$ so that $q h^{-1} = \sigma_\eta^2$.

Then our error terms can be written:

\[\varepsilon_t \sim N(0, h^{-1}) \\ \eta_t \sim N(0, q h^{-1}) \\\]And the true values are:

- $h_0^{-1} = 1 / 3 = 0.33$

- $q = 10 / 3 = 3.33$

| To take a Bayesian approach to this problem, we assume that $\psi$ is a random variable, and we want to learn about the values of $\psi$ based on the data $Y_T$; in fact we want a density $p(\psi | Y_T)$. To do this, we use Bayes rule to write: |

or

\[\underbrace{p(\psi | Y_T)}_{\text{posterior}} \propto \underbrace{p(Y_T | \psi)}_{\text{likelihood}} \underbrace{p(\psi)}_{\text{prior}}\]The object of interest is the posterior; to achieve it we need to specify a prior density for the unknown parameters and the likelihood function of the model.

Prior

We will use the following priors:

Precision

Since the precision must be positive, but has no theoretical upper bound, we use a Gamma prior:

\[h \sim \text{Gamma}(\alpha_h, \beta_h)\]to be specific, the density is written:

\[p(h) = \frac{\beta_h^{\alpha_h}}{\Gamma(\alpha)} h^{\alpha_h-1}e^{-\beta_h h}\]and we set the hyperparameters as $\alpha_h = 2, \beta_h = 2$. In this case, we have $E(h) = \alpha_h / \beta_h = 1$ and also $E(h^{-1}) = E(\sigma_\varepsilon^2) = 1$.

Ratio of variances

Similarly, the ratio of variances must be positive, but has no theoretical upper bound, so we again use an (independent) Gamma prior:

\[q \sim \text{Gamma}(\alpha_q, \beta_q)\]and we set the same hyperparameters, so $\alpha_q = 2, \beta_q = 2$. Since $E(q) = 1$, our prior is of equal variances. We then have $E(\sigma_\eta^2) = E(q h^{-1}) = E(q) E(h^{-1}) = 1$.

Initial state prior

As noted above, the Kalman filter must be initialized with $\mu_0 \sim N(m_0, P_0)$. We will use the following approximately diffuse prior:

\[\mu_0 \sim N(0, 10^6)\]Likelihood

For given parameters, likelihood of this model can be calculated via prediction error decomposition using an application of the Kalman filter iterations.

Posterior Simulation: Metropolis-Hastings

One option for describing the posterior is via MCMC posterior simulation methods. The Metropolis-Hastings algorthm is simple and only requires the ability to evaluate the prior densities and the likelihood. The priors have known densities, and the likelihood function can be computed using the state space models from the Statsmodels tsa.statespace package. We will use the PyMC package to streamline specification of priors and sampling in the Metropolis-Hastings case.

The statespace package is meant to make it easy to specify and evaluate state space models. Below, we create a new LocalLevel class. Among other things, it inherits from MLEModel a loglike method which we can use to evaluate the likelihood at various parameters.

# Priors

precision = mc.Gamma('precision', 2, 4)

ratio = mc.Gamma('ratio', 2, 1)

# Likelihood calculated using the state-space model

class LocalLevel(sm.tsa.statespace.MLEModel):

def __init__(self, endog):

# Initialize the state space model

super(LocalLevel, self).__init__(endog, k_states=1,

initialization='approximate_diffuse',

loglikelihood_burn=1)

# Initialize known components of the state space matrices

self.ssm['design', :] = 1

self.ssm['transition', :] = 1

self.ssm['selection', :] = 1

@property

def start_params(self):

return [1. / np.var(self.endog), 1.]

@property

def param_names(self):

return ['h_inv', 'q']

def update(self, params, transformed=True, **kwargs):

params = super(LocalLevel, self).update(params, transformed, **kwargs)

h, q = params

sigma2_eps = 1. / h

sigma2_eta = q * sigma2_eps

self.ssm['obs_cov', 0, 0] = sigma2_eps

self.ssm['state_cov', 0, 0] = sigma2_eta

# Instantiate the local level model with our simulated data

ll_mod = LocalLevel(y)

ll_mod.filter(ll_mod.start_params)

# Create the stochastic (observed) component

@mc.stochastic(dtype=LocalLevel, observed=True)

def local_level(value=ll_mod, h=precision, q=ratio):

return value.loglike([h, q], transformed=True)

# Create the PyMC model

ll_mc = mc.Model((precision, ratio, local_level))

# Create a PyMC sample

ll_sampler = mc.MCMC(ll_mc)

Bayesian Estimation: Metropolis-Hastings

Now that we have specified our priors and likelihood, and wrapped it up in a PyMC Model and MCMC sampler, we can easily sample from the posterior.

# Sample

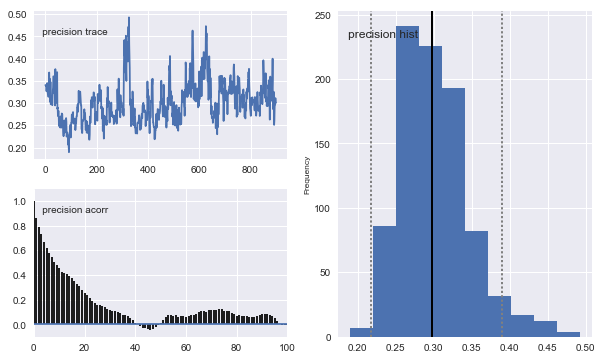

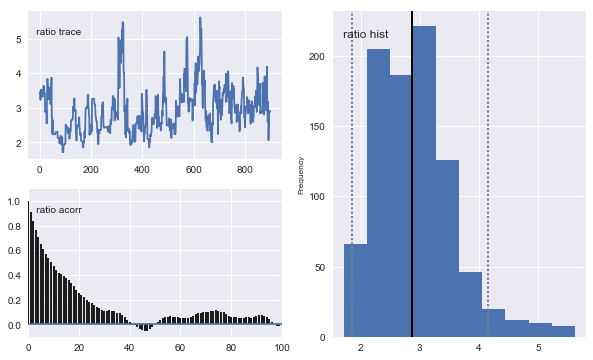

ll_sampler.sample(iter=10000, burn=1000, thin=10)

# Plot traces

mc.Matplot.plot(ll_sampler)

[-----------------100%-----------------] 10000 of 10000 complete in 20.6 secPlotting precision

Plotting ratio

Notice that the means of the posterior densities are close to the true values of the parameters.

Classical Estimation

In addition to defining the state space models, Statsmodels allows easy estimation of parameters via maximum likelihood. For comparison, here is the output from MLE:

ll_res = ll_mod.fit()

print ll_res.summary()

Statespace Model Results

==============================================================================

Dep. Variable: y No. Observations: 1000

Model: LocalLevel Log Likelihood -2789.529

Date: Sun, 22 Jan 2017 AIC 5583.058

Time: 14:20:17 BIC 5592.873

Sample: 0 HQIC 5586.788

- 1000

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

h_inv 0.3045 0.049 6.196 0.000 0.208 0.401

q 2.9588 0.690 4.289 0.000 1.607 4.311

===================================================================================

Ljung-Box (Q): 37.10 Jarque-Bera (JB): 1.83

Prob(Q): 0.60 Prob(JB): 0.40

Heteroskedasticity (H): 0.93 Skew: 0.03

Prob(H) (two-sided): 0.54 Kurtosis: 3.20

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

These also closely match the true parameter values.

Alternate Model: ARIMA(0,1,1)

It can be shown (see e.g. Harvey (1989), among many others) that the local level model is equivalent to an ARIMA(0,1,1) model, which is written:

\[\Delta y_t = \theta \zeta_{t-1} + \zeta_t, \qquad \zeta_t \sim N(0, \sigma_\zeta^2)\]It is important to note that $\sigma_\zeta^2$ here is not equivalent to $\sigma_\varepsilon^2$ from the local level model. However, we can connect the models through $q = - (1 + \theta)^2 / \theta$. Note that to generate a valid $q$, $\theta$ must be negative.

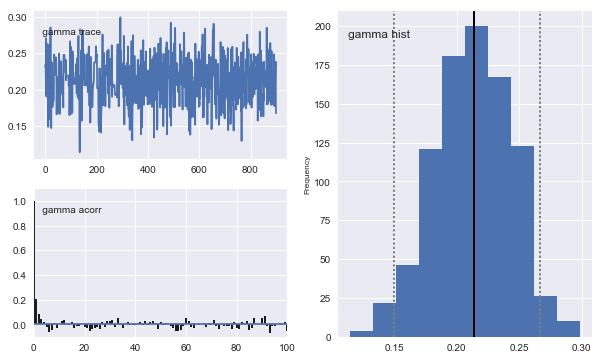

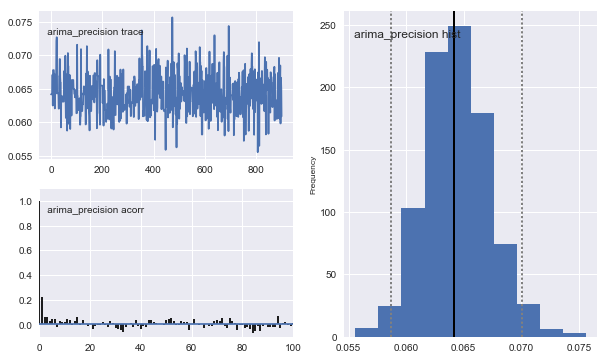

We will use the same Gamma prior as above on the precision $h^{-1} = \sigma_\eta^2$, but we must specify a new prior for $\theta$. We will specify that $-\theta \equiv \gamma \sim \text{Beta}(\alpha_\theta, \beta_\theta)$. Since the entire support for the Beta distribution falls between 0 and 1, this prior implies $\theta \in [-1, 0]$. We would expect that $\hat \theta \approx -0.21$, since then $q = \frac{-(1 - 0.21)^2}{-0.21} \approx 3$ (and so $\hat \gamma \approx 0.21$).

Above, we defined a new state space model (LocalLevel), but we can also use built-in models if the one we want is available. Statsmodels has a statespace.SARIMAX class that can handle the specification and likelihood evaluation for an ARIMA(0,1,1) model, and we can simply instantiate it here.

# Priors

arima_precision = mc.Gamma('arima_precision', 2, 4)

gamma = mc.Beta('gamma', 2, 1)

# Instantiate the ARIMA model with our simulated data

arima_mod = sm.tsa.SARIMAX(y, order=(0,1,1))

# Create the stochastic (observed) component

@mc.stochastic(dtype=sm.tsa.SARIMAX, observed=True)

def arima(value=arima_mod, h=arima_precision, gamma=gamma):

# Rejection sampling

if gamma < 0 or h < 0:

return 0

return value.loglike(np.r_[-gamma, 1./h], transformed=True)

# Create the PyMC model

arima_mc = mc.Model((arima_precision, gamma, arima))

# Create a PyMC sample

arima_sampler = mc.MCMC(arima_mc)

Bayesian Estimation: Metropolis-Hastings

# Sample

arima_sampler.sample(iter=10000, burn=1000, thin=10)

# Plot traces

mc.Matplot.plot(arima_sampler)

[-----------------100%-----------------] 10000 of 10000 complete in 29.1 secPlotting gamma

Plotting arima_precision

Classical Estimation

arima_res = arima_mod.fit()

print arima_res.summary()

Statespace Model Results

==============================================================================

Dep. Variable: y No. Observations: 1000

Model: SARIMAX(0, 1, 1) Log Likelihood -2789.529

Date: Sun, 22 Jan 2017 AIC 5583.058

Time: 14:20:48 BIC 5592.873

Sample: 0 HQIC 5586.788

- 1000

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

ma.L1 -0.2106 0.032 -6.576 0.000 -0.273 -0.148

sigma2 15.5913 0.667 23.386 0.000 14.285 16.898

===================================================================================

Ljung-Box (Q): 37.10 Jarque-Bera (JB): 1.83

Prob(Q): 0.60 Prob(JB): 0.40

Heteroskedasticity (H): 0.93 Skew: 0.03

Prob(H) (two-sided): 0.54 Kurtosis: 3.20

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

Forecasts

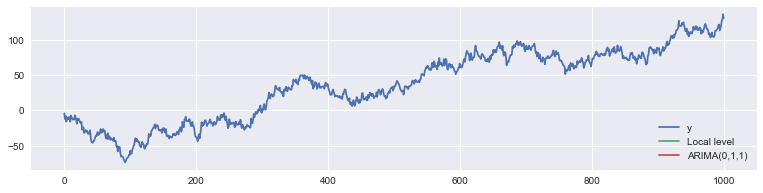

To see that the models are the same, we can check that they make the same one-step-ahead predictions.

fig, ax = plt.subplots(figsize=(13,3))

ax.plot(y, label='y')

ax.plot(ll_res.predict()[0], label='Local level')

ax.plot(arima_res.predict()[0], label='ARIMA(0,1,1)')

ax.legend(loc='lower right');

In fact they’re so close, it’s hard to visually see just how close they are:

print(np.max(np.abs(arima_res.predict()[0] - ll_res.predict()[0])))

0.0