Estimating a Real Business Cycle DSGE Model by Maximum Likelihood in Python(Open on Google Colab | View / download notebook | Report a problem)

Note: this page was updated on October 26, 2016.

Table of Contents

Estimating a Real Business Cycle DSGE Model by Maximum Likelihood in Python

This notebook demonstrates how to setup, solve, and estimate a simple real business cycle model in Python. The model is very standard; the setup and notation here is a hybrid of Ruge-Murcia (2007) and DeJong and Dave (2011).

Since we will be proceeding step-by-step, the code will match that progression by generating a series of child classes, so that we can add the functionality step-by-step. Of course, in practice a single class incorporating all the functionality would be all you would need.

%matplotlib inline

from __future__ import division

import numpy as np

from scipy import optimize, signal

import pandas as pd

from pandas_datareader.data import DataReader

import statsmodels.api as sm

from statsmodels.tools.numdiff import approx_fprime, approx_fprime_cs

from IPython.display import display

import matplotlib.pyplot as plt

# import seaborn as sn

from numpy.testing import assert_allclose

# Set some pretty-printing options

np.set_printoptions(precision=3, suppress=True, linewidth=120)

pd.set_option('float_format', lambda x: '%.3g' % x, )

Household problem

\[\max E_0 \sum_{t=0}^\infty \beta^t u(c_t, l_t)\]subject to:

- the budget constraint: $y_t = c_t + i_t$

- the capital accumulation equation: $k_{t+1} = (1 - \delta) k_t + i_t$

- $1 = l_t + n_t$

where households have the following production technology:

\[y_t = z_t f(k_t, n_t)\]and where the (log of the) technology process follows an AR(1) process:

\[\log z_t = \rho \log z_{t-1} + \varepsilon_t, \qquad \varepsilon_t \sim N(0, \sigma^2)\]Functional forms

We will assume additively separable utility in consumption and leisure, with:

\[u(c_t, n_t) = \log(c_t) + \psi l_t\]where $\psi$ is a scalar weight.

The production function will be Cobb-Douglas:

\[f(k_t, n_t) = k_t^\alpha n_t^{1 - \alpha}\]Optimal behavior

Optimal household behavior is standard:

\[\begin{align} \psi & = \frac{1}{c_t} (1 - \alpha) z_t \left ( \frac{k_t}{n_t} \right )^{\alpha} \\ \frac{1}{c_t} & = \beta E_t \left \{ \frac{1}{c_{t+1}} \left [ \alpha z_{t+1} \left ( \frac{k_{t+1}}{n_{t+1}} \right )^{\alpha - 1} + (1 - \delta) \right ] \right \} \\ \end{align}\]Nonlinear system

Collecting all of the model equations, we have:

\[\begin{align} \psi c_t & = (1 - \alpha) z_t \left ( \frac{k_t}{n_t} \right )^{\alpha} & \text{Static FOC} \\ \frac{1}{c_t} & = \beta E_t \left \{ \frac{1}{c_{t+1}} \left [ \alpha z_{t+1} \left ( \frac{k_{t+1}}{n_{t+1}} \right )^{\alpha - 1} + (1 - \delta) \right ] \right \} & \text{Euler equation} \\ y_t & = z_t k_t^\alpha n_t^{1 - \alpha} & \text{Production function} \\ y_t & = c_t + i_t & \text{Aggregate resource constraint} \\ k_{t+1} & = (1 - \delta) k_t + i_t & \text{Captial accumulation} \\ 1 & = l_t + n_t & \text{Labor-leisure tradeoff} \\ \log z_t & = \rho \log z_{t-1} + \varepsilon_t & \text{Technology shock transition} \end{align}\]Variables / Parameters

This system is in the following variables:

\[\begin{align} x_t = \{ \quad & &\\ & y_t, & \text{Output}\\ & c_t, & \text{Consumption}\\ & i_t, & \text{Investment}\\ & n_t, & \text{Labor}\\ & l_t, & \text{Leisure}\\ & k_t, & \text{Capital}\\ & z_t & \text{Technology} \\ \} \quad & & \end{align}\]and depends on the following parameters:

\[\begin{align} \{ \quad & &\\ & \beta, & \text{Discount rate}\\ & \psi, & \text{Marginal disutility of labor}\\ & \delta, & \text{Depreciation rate}\\ & \alpha, & \text{Capital-share of output}\\ & \rho, & \text{Technology shock persistence}\\ & \sigma^2 & \text{Technology shock variance}\\ \} \quad & & \end{align}\]# Save the names of the equations, variables, and parameters

equation_names = [

'static FOC', 'euler equation', 'production',

'aggregate resource constraint', 'capital accumulation',

'labor-leisure', 'technology shock transition'

]

variable_names = [

'output', 'consumption', 'investment',

'labor', 'leisure', 'capital', 'technology'

]

parameter_names = [

'discount rate', 'marginal disutility of labor',

'depreciation rate', 'capital share',

'technology shock persistence',

'technology shock standard deviation',

]

# Save some symbolic forms for pretty-printing

variable_symbols = [

r"y", r"c", r"i", r"n", r"l", r"k", r"z",

]

contemporaneous_variable_symbols = [

r"$%s_t$" % symbol for symbol in variable_symbols

]

lead_variable_symbols = [

r"$%s_{t+1}$" % symbol for symbol in variable_symbols

]

parameter_symbols = [

r"$\beta$", r"$\psi$", r"$\delta$", r"$\alpha$", r"$\rho$", r"$\sigma^2$"

]

Numerical method

Using these equations, we can numerically find the steady-state using a root-finding algorithm and can then log-linearize around the steady-state using a numerical gradient procedure. In particular, here we follow DeJong and Dave (2011) chapter 2 and 3.1.

Write the generic non-linear system as:

\[\Gamma(E_t x_{t+1}, x_t, z_t) = 0\]in the absense of shocks, this can be rewritten as:

\[\Psi(x_{t+1}, x_t) = 0\]or as:

\[\Psi_1(x_{t+1}, x_t) = \Psi_2(x_{t+1}, x_t)\]and finally in logs as

\[\log \Psi_1(e^{\log x_{t+1}}, e^{\log x_t}) - \log \Psi_2(e^{\log x_{t+1}}, e^{\log x_t}) = 0\]First, we define a new class (RBC1) which holds the state of the RBC model (its dimensions, parameters, etc) and has methods for evaluating the log system. The eval_logged method evaluates the last equation, above.

Notice that the order of variables and order of equations is as described above.

class RBC1(object):

def __init__(self, params=None):

# Model dimensions

self.k_params = 6

self.k_variables = 7

# Initialize parameters

if params is not None:

self.update(params)

def update(self, params):

# Save deep parameters

self.discount_rate = params[0]

self.disutility_labor = params[1]

self.depreciation_rate = params[2]

self.capital_share = params[3]

self.technology_shock_persistence = params[4]

self.technology_shock_std = params[5]

def eval_logged(self, log_lead, log_contemporaneous):

(log_lead_output, log_lead_consumption, log_lead_investment,

log_lead_labor, log_lead_leisure, log_lead_capital,

log_lead_technology_shock) = log_lead

(log_output, log_consumption, log_investment, log_labor,

log_leisure, log_capital, log_technology_shock) = log_contemporaneous

return np.r_[

self.log_static_foc(

log_lead_consumption, log_lead_labor,

log_lead_capital, log_lead_technology_shock

),

self.log_euler_equation(

log_lead_consumption, log_lead_labor,

log_lead_capital, log_lead_technology_shock,

log_consumption

),

self.log_production(

log_lead_output, log_lead_labor, log_lead_capital,

log_lead_technology_shock

),

self.log_aggregate_resource_constraint(

log_lead_output, log_lead_consumption,

log_lead_investment

),

self.log_capital_accumulation(

log_lead_capital, log_investment, log_capital

),

self.log_labor_leisure_constraint(

log_lead_labor, log_lead_leisure

),

self.log_technology_shock_transition(

log_lead_technology_shock, log_technology_shock

)

]

def log_static_foc(self, log_lead_consumption, log_lead_labor,

log_lead_capital, log_lead_technology_shock):

return (

np.log(self.disutility_labor) +

log_lead_consumption -

np.log(1 - self.capital_share) -

log_lead_technology_shock -

self.capital_share * (log_lead_capital - log_lead_labor)

)

def log_euler_equation(self, log_lead_consumption, log_lead_labor,

log_lead_capital, log_lead_technology_shock,

log_consumption):

return (

-log_consumption -

np.log(self.discount_rate) +

log_lead_consumption -

np.log(

(self.capital_share *

np.exp(log_lead_technology_shock) *

np.exp((1 - self.capital_share) * log_lead_labor) /

np.exp((1 - self.capital_share) * log_lead_capital)) +

(1 - self.depreciation_rate)

)

)

def log_production(self, log_lead_output, log_lead_labor, log_lead_capital,

log_lead_technology_shock):

return (

log_lead_output -

log_lead_technology_shock -

self.capital_share * log_lead_capital -

(1 - self.capital_share) * log_lead_labor

)

def log_aggregate_resource_constraint(self, log_lead_output, log_lead_consumption,

log_lead_investment):

return (

log_lead_output -

np.log(np.exp(log_lead_consumption) + np.exp(log_lead_investment))

)

def log_capital_accumulation(self, log_lead_capital, log_investment, log_capital):

return (

log_lead_capital -

np.log(np.exp(log_investment) + (1 - self.depreciation_rate) * np.exp(log_capital))

)

def log_labor_leisure_constraint(self, log_lead_labor, log_lead_leisure):

return (

-np.log(np.exp(log_lead_labor) + np.exp(log_lead_leisure))

)

def log_technology_shock_transition(self, log_lead_technology_shock, log_technology_shock):

return (

log_lead_technology_shock -

self.technology_shock_persistence * log_technology_shock

)

Later we will estimate (some of) the parameters; in the meantime we fix them at the values used to generate the datasets in Ruge-Murcia (2007).

# Setup fixed parameters

parameters = pd.DataFrame({

'name': parameter_names,

'value': [0.95, 3, 0.025, 0.36, 0.85, 0.04]

})

parameters.T

| 0 | 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|---|

| name | discount rate | marginal disutility of labor | depreciation rate | capital share | technology shock persistence | technology shock standard deviation |

| value | 0.95 | 3 | 0.025 | 0.36 | 0.85 | 0.04 |

Steady state

Numeric calculation

To numerically calculate steady-state, we apply a root-finding algorithm to the eval_logged method. In particular, we are finding values $\bar x$ such that

These will be confirmed analytically, below.

Here we create a derived class, RBC2 which extends all of the functionality from above, but now includes methods for numerical calcualtion of the steady-state.

class RBC2(RBC1):

def steady_state_numeric(self):

# Setup starting parameters

log_start_vars = [0.5] * self.k_variables # very arbitrary

# Setup the function the evaluate

eval_logged = lambda log_vars: self.eval_logged(log_vars, log_vars)

# Apply the root-finding algorithm

result = optimize.root(eval_logged, log_start_vars)

return np.exp(result.x)

mod2 = RBC2(parameters['value'])

steady_state = pd.DataFrame({

'value': mod2.steady_state_numeric()

}, index=variable_names)

steady_state.T

| output | consumption | investment | labor | leisure | capital | technology | |

|---|---|---|---|---|---|---|---|

| value | 0.572 | 0.506 | 0.0663 | 0.241 | 0.759 | 2.65 | 1 |

Analytic evaluation

In this case, we can analytically evaluate the steady-state:

\[\begin{align} \frac{\bar y}{\bar n} & = \eta \\ \frac{\bar c}{\bar n} & = \eta - \delta \theta \\ \frac{\bar i}{\bar n} & = \delta \theta \\ \bar n & = \frac{1}{\left ( \frac{1}{1 - \alpha} \right ) \psi \left [ 1 - \delta \theta^{1-\alpha} \right ]} \\ \bar l & = 1 - \bar n \\ \frac{\bar k}{\bar n} & = \theta \end{align}\]where \(\begin{align} \theta & = \left ( \frac{\alpha}{1/\beta - (1 - \delta)} \right )^\frac{1}{1-\alpha} \\ \eta & = \theta^\alpha \end{align}\)

class RBC3(RBC2):

def update(self, params):

# Update the deep parameters

super(RBC3, self).update(params)

# And now also calculate some intermediate parameters

self.theta = (self.capital_share / (

1 / self.discount_rate -

(1 - self.depreciation_rate)

))**(1 / (1 - self.capital_share))

self.eta = self.theta**self.capital_share

def steady_state_analytic(self):

steady_state = np.zeros(7)

# Labor (must be computed first)

numer = (1 - self.capital_share) / self.disutility_labor

denom = (1 - self.depreciation_rate * self.theta**(1 - self.capital_share))

steady_state[3] = numer / denom

# Output

steady_state[0] = self.eta * steady_state[3]

# Consumption

steady_state[1] = (1 - self.capital_share) * self.eta / self.disutility_labor

# Investment

steady_state[2] = self.depreciation_rate * self.theta * steady_state[3]

# Labor (computed already)

# Leisure

steady_state[4] = 1 - steady_state[3]

# Capital

steady_state[5] = self.theta * steady_state[3]

# Technology shock

steady_state[6] = 1

return steady_state

mod3 = RBC3(parameters['value'])

steady_state = pd.DataFrame({

'numeric': mod3.steady_state_numeric(),

'analytic': mod3.steady_state_analytic()

}, index=variable_names)

steady_state.T

| output | consumption | investment | labor | leisure | capital | technology | |

|---|---|---|---|---|---|---|---|

| numeric | 0.572 | 0.506 | 0.0663 | 0.241 | 0.759 | 2.65 | 1 |

| analytic | 0.572 | 0.506 | 0.0663 | 0.241 | 0.759 | 2.65 | 1 |

Log-linearization

The system we wrote down, above, was non-linear. In order to estimate it, we want to get it in a linear form:

\[A E_t \tilde x_{t+1} = B \tilde x_{t} + C v_{t+1}\]where $v_{t+1}$ contains structural shocks (here, $z_t$ is included in the $x_t$ vector, and the only structural shock is $\varepsilon_t$, the innovation to $z_t$).

This can be achieved via log-linearization around the steady state. In this case, DeJong and Dave (2011) show that:

\[A = \left [ \frac{\partial \log [ \Psi_1 ]}{\partial \log(x_{t+1})} (\bar x) - \frac{\partial \log [ \Psi_2 ]}{\partial \log(x_{t+1})} (\bar x) \right ] \\ B = - \left [ \frac{\partial \log [ \Psi_1 ]}{\partial \log(x_t)} (\bar x) - \frac{\partial \log [ \Psi_2 ]}{\partial \log(x_t)} (\bar x) \right ] \\\]where $\tilde x_t = \log \left ( \frac{x_t}{\bar x} \right )$ expresses the variables in proportional deviation from steady-state form.

The matrix $C$ can be constructed by observation. In this case, we have:

\[C = \begin{bmatrix} 0 & 0 & 0 & 0 & 0 & 0 & 1 \end{bmatrix} \qquad \text{and} \qquad v_{t+1} \equiv \varepsilon_t\]Numeric calculation

Since the eval_logged method of our class evaluates $\log \Psi_1(e^{\log x_{t+1}}, e^{\log x_t}) - \log \Psi_2(e^{\log x_{t+1}}, e^{\log x_t})$, we can apply a numerical gradient procedure to it to get $A$, when we differentiate with respect to the lead variables, and $B$, when we differentiate with respect to the contemporaneous variables.

class RBC4(RBC3):

def A_numeric(self):

log_steady_state = np.log(self.steady_state_analytic())

eval_logged_lead = lambda log_lead: self.eval_logged(log_lead, log_steady_state)

return approx_fprime_cs(log_steady_state, eval_logged_lead)

def B_numeric(self):

log_steady_state = np.log(self.steady_state_analytic())

eval_logged_contemporaneous = lambda log_contemp: self.eval_logged(log_steady_state, log_contemp)

return -approx_fprime_cs(log_steady_state, eval_logged_contemporaneous)

def C(self):

return np.r_[[0]*(self.k_variables-1), 1]

mod4 = RBC4(parameters['value'])

display(pd.DataFrame(mod4.A_numeric(), index=equation_names, columns=lead_variable_symbols))

display(pd.DataFrame(mod4.B_numeric(), index=equation_names, columns=contemporaneous_variable_symbols))

display(pd.DataFrame(mod4.C(), index=equation_names, columns=[r'$\varepsilon_t$']))

| $y_{t+1}$ | $c_{t+1}$ | $i_{t+1}$ | $n_{t+1}$ | $l_{t+1}$ | $k_{t+1}$ | $z_{t+1}$ | |

|---|---|---|---|---|---|---|---|

| static FOC | 0 | 1 | 0 | 0.36 | 0 | -0.36 | -1 |

| euler equation | 0 | 1 | 0 | -0.0472 | 0 | 0.0472 | -0.0737 |

| production | 1 | 0 | 0 | -0.64 | 0 | -0.36 | -1 |

| aggregate resource constraint | 1 | -0.884 | -0.116 | 0 | 0 | 0 | 0 |

| capital accumulation | 0 | 0 | 0 | 0 | 0 | 1 | 0 |

| labor-leisure | -0 | -0 | -0 | -0.241 | -0.759 | -0 | -0 |

| technology shock transition | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| $y_t$ | $c_t$ | $i_t$ | $n_t$ | $l_t$ | $k_t$ | $z_t$ | |

|---|---|---|---|---|---|---|---|

| static FOC | -0 | -0 | -0 | -0 | -0 | -0 | -0 |

| euler equation | -0 | 1 | -0 | -0 | -0 | -0 | -0 |

| production | -0 | -0 | -0 | -0 | -0 | -0 | -0 |

| aggregate resource constraint | -0 | -0 | -0 | -0 | -0 | -0 | -0 |

| capital accumulation | -0 | -0 | 0.025 | -0 | -0 | 0.975 | -0 |

| labor-leisure | -0 | -0 | -0 | -0 | -0 | -0 | -0 |

| technology shock transition | -0 | -0 | -0 | -0 | -0 | -0 | 0.85 |

| $\varepsilon_t$ | |

|---|---|

| static FOC | 0 |

| euler equation | 0 |

| production | 0 |

| aggregate resource constraint | 0 |

| capital accumulation | 0 |

| labor-leisure | 0 |

| technology shock transition | 1 |

Analytic evaluation

This system can be log-linearized directly, as well, yielding (see e.g. Ruge-Murcia (2007) Appendix A for these formulas, with slightly different notation):

\[\begin{align} \tilde c_t & = \tilde z_t + \alpha \tilde k_t - \alpha \tilde n_t \\ -\tilde c_t & = -E_t \tilde c_{t+1} + \zeta (\alpha - 1) E_t \tilde k_{t+1} + \zeta (1 - \alpha) E_t \tilde n_{t+1} + \zeta E_t \tilde z_{t+1} \\ \tilde y_t & = \tilde z_t + \alpha \tilde k_t + (1 - \alpha) \tilde n_t \\ \tilde y_t & = \gamma \tilde c_t + (1 - \gamma) \tilde i_t \\ \tilde k_{t+1} & = (1 - \delta) \tilde k_t + \delta \tilde i_t \\ 0 & = \frac{\bar l}{\bar l + \bar n} \tilde l_{t+1} + \frac{\bar n}{\bar l + \bar n} \tilde n_{t+1} \\ \tilde z_{t+1} & = \rho \tilde z_t + \varepsilon_t \end{align}\]where $\zeta = \alpha \beta \theta^{\alpha - 1}$ and $\gamma = 1 - \delta \theta^{1 - \alpha}$ is the steady-state consumption-output ratio.

class RBC5(RBC4):

def update(self, params):

super(RBC5, self).update(params)

# Now calculate some more intermediate parameters

self.gamma = 1 - self.depreciation_rate * self.theta**(1 - self.capital_share)

self.zeta = self.capital_share * self.discount_rate * self.theta**(self.capital_share - 1)

def A_analytic(self):

steady_state = self.steady_state_analytic()

A = np.array([

[0, 1, 0, self.capital_share, 0, -self.capital_share, -1],

[0, 1, 0, self.zeta * (self.capital_share - 1), 0, self.zeta * (1 - self.capital_share), -self.zeta],

[1, 0, 0, (self.capital_share - 1), 0, -self.capital_share, -1],

[1, -self.gamma, (self.gamma - 1), 0, 0, 0, 0],

[0, 0, 0, 0, 0, 1, 0],

[0, 0, 0, -steady_state[3], -steady_state[4], 0, 0],

[0, 0, 0, 0, 0, 0, 1],

])

return A

def B_analytic(self):

B = np.array([

[0, 0, 0, 0, 0, 0, 0],

[0, 1, 0, 0, 0, 0, 0],

[0, 0, 0, 0, 0, 0, 0],

[0, 0, 0, 0, 0, 0, 0],

[0, 0, self.depreciation_rate, 0, 0, 1 - self.depreciation_rate, 0],

[0, 0, 0, 0, 0, 0, 0],

[0, 0, 0, 0, 0, 0, self.technology_shock_persistence],

])

return B

mod5 = RBC5(parameters['value'])

display(pd.DataFrame(mod5.A_analytic(), index=equation_names, columns=lead_variable_symbols))

assert(np.all(np.abs(mod5.A_numeric() - mod5.A_analytic()) < 1e-10))

display(pd.DataFrame(mod5.B_analytic(), index=equation_names, columns=lead_variable_symbols))

assert(np.all(np.abs(mod5.B_numeric() - mod5.B_analytic()) < 1e-10))

| $y_{t+1}$ | $c_{t+1}$ | $i_{t+1}$ | $n_{t+1}$ | $l_{t+1}$ | $k_{t+1}$ | $z_{t+1}$ | |

|---|---|---|---|---|---|---|---|

| static FOC | 0 | 1 | 0 | 0.36 | 0 | -0.36 | -1 |

| euler equation | 0 | 1 | 0 | -0.0472 | 0 | 0.0472 | -0.0737 |

| production | 1 | 0 | 0 | -0.64 | 0 | -0.36 | -1 |

| aggregate resource constraint | 1 | -0.884 | -0.116 | 0 | 0 | 0 | 0 |

| capital accumulation | 0 | 0 | 0 | 0 | 0 | 1 | 0 |

| labor-leisure | 0 | 0 | 0 | -0.241 | -0.759 | 0 | 0 |

| technology shock transition | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| $y_{t+1}$ | $c_{t+1}$ | $i_{t+1}$ | $n_{t+1}$ | $l_{t+1}$ | $k_{t+1}$ | $z_{t+1}$ | |

|---|---|---|---|---|---|---|---|

| static FOC | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| euler equation | 0 | 1 | 0 | 0 | 0 | 0 | 0 |

| production | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| aggregate resource constraint | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| capital accumulation | 0 | 0 | 0.025 | 0 | 0 | 0.975 | 0 |

| labor-leisure | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| technology shock transition | 0 | 0 | 0 | 0 | 0 | 0 | 0.85 |

System reduction

The system currently has 7 equations in 7 unknowns. This can be reduced into a system of 3 equations in 3 unknowns (consumption, capital, and the technology shock), by substituting out output, investment, labor, and leisure. Given a solution to the reduced system, the remaining four unknowns can be calculated. Also, we remove the technology shock transition from the state vector and include it instead in the stochastic shocks component $(v_{t+1})$.

First, notice that (using the static first order condition, production function, aggregate resource constraint, and labor-leisure tradeoff equations, respectively):

\[\begin{align} \tilde n_t & = - \frac{1}{\alpha} \tilde c_t + \frac{1}{\alpha} \tilde z_t + \tilde k_t \\ \tilde y_t & = \tilde z_t + \alpha \tilde k_t + (1 - \alpha) \left [ - \frac{1}{\alpha} \tilde c_t + \frac{1}{\alpha} \tilde z_t + \tilde k_t \right ] \\ & = \frac{1}{\alpha} \tilde z_t - \frac{1 - \alpha}{\alpha} \tilde c_t + \tilde k_t \\ \tilde i_t & = \frac{1}{1 - \gamma} \left [ \frac{1}{\alpha} \tilde z_t - \frac{1 - \alpha}{\alpha} \tilde c_t + \tilde k_t - \gamma \tilde c_t \right ] \\ & = \frac{1}{1 - \gamma} \left [ \frac{1}{\alpha} \tilde z_t - \frac{1 - \alpha + \gamma \alpha}{\alpha} \tilde c_t + \tilde k_t \right ] \\ \tilde l_t & = - \frac{\bar n}{1 - \bar n} \tilde n_t \end{align}\]then we can plug these values into the remaining three equations (Euler, capital accumulation, and shock transition equations):

\[\begin{align} k_{t+1} & = (1 - \delta) \tilde k_t + \delta \frac{1}{1 - \gamma} \left [ \frac{1}{\alpha} \tilde z_t - \frac{1 - \alpha + \gamma \alpha}{\alpha} \tilde c_t + \tilde k_t \right ] \\ & = \underbrace{\left [ 1 + \delta \left ( \frac{\gamma}{1 - \gamma} \right ) \right ]}_{B_{11}, F_{11}} \tilde k_t + \underbrace{\frac{-\delta (1 - \alpha + \gamma \alpha)}{\alpha (1 - \gamma)}}_{B_{12}, F_{12}} \tilde c_t + \underbrace{\frac{\delta}{\alpha (1 - \gamma)}}_{C_1, G_{12}} \tilde z_t \end{align}\]and

\[\begin{align} E_t \tilde c_{t+1} & = \tilde c_t + \zeta (\alpha - 1) E_t k_{t+1} + \zeta (1 - \alpha) E_t \left [ - \frac{1}{\alpha} \tilde c_{t+1} + \frac{1}{\alpha} \tilde z_{t+1} + \tilde k_{t+1} \right ] + \zeta E_t \tilde z_{t+1} \\ & = \tilde c_t + \zeta (\alpha - 1) E_t \tilde k_{t+1} - \zeta \frac{(1 - \alpha)}{\alpha} E_t \tilde c_{t+1} + \zeta \frac{(1 - \alpha)}{\alpha} E_t z_{t+1} + \zeta (1 - \alpha) E_t \tilde k_{t+1} + \zeta E_t \tilde z_{t+1} \\ & = \underbrace{\frac{\alpha}{\zeta + \alpha (1 - \zeta)}}_{B_{22}} \tilde c_t + \underbrace{\frac{\zeta \rho}{\zeta + \alpha (1 - \zeta )}}_{C_2} \tilde z_t \end{align}\]and

\[\begin{align} \tilde z_{t+1} & = \rho \tilde z_t + \varepsilon_t \end{align}\]# Save the names of the equations, variables, and parameters

# in the reduced model

reduced_equation_names = [

'euler equation', 'capital accumulation'

]

reduced_variable_names = [

'consumption', 'capital'

]

reduced_parameter_names = parameter_names

# Save some symbolic forms for pretty-printing

reduced_variable_symbols = [

r"c", r"k"

]

reduced_contemporaneous_variable_symbols = [

r"$%s_t$" % symbol for symbol in reduced_variable_symbols

]

reduced_lead_variable_symbols = [

r"$%s_{t+1}$" % symbol for symbol in reduced_variable_symbols

]

reduced_parameter_symbols = parameter_symbols

class ReducedRBC1(RBC5):

def __init__(self, params=None):

# Model dimensions

self.k_params = 6

self.k_variables = 2

# Index for the reduced form variables

self.reduced_idx = [1, -2]

# Initialize parameters

if params is not None:

self.update(params)

def steady_state_numeric(self):

return super(ReducedRBC1, self).steady_state_numeric()[self.reduced_idx]

def steady_state_analytic(self):

return super(ReducedRBC1, self).steady_state_analytic()[self.reduced_idx]

def A(self):

return np.eye(self.k_variables)

def B(self):

B11 = 1 + self.depreciation_rate * (self.gamma / (1 - self.gamma))

B12 = (

-self.depreciation_rate *

(1 - self.capital_share + self.gamma * self.capital_share) /

(self.capital_share * (1 - self.gamma))

)

B21 = 0

B22 = self.capital_share / (self.zeta + self.capital_share*(1 - self.zeta))

return np.array([[B11, B12],

[B21, B22]])

def C(self):

C1 = self.depreciation_rate / (self.capital_share * (1 - self.gamma))

C2 = (

self.zeta * self.technology_shock_persistence /

(self.zeta + self.capital_share*(1 - self.zeta))

)

return np.array([C1, C2])[:,np.newaxis]

# Setup the model

reduced_mod1 = ReducedRBC1(parameters['value'])

# Display the steady-states

reduced_steady_state = pd.DataFrame({

'steady state': reduced_mod1.steady_state_analytic()

}, index=reduced_variable_names)

display(reduced_steady_state.T)

# Test the model coefficients for accuracy

# (results from "Emsm", downloaded from

# https://sites.google.com/site/frugemurcia/home/replication-files

# on 06/19/2015)

assert_allclose(

reduced_mod1.B(),

np.array([[1.1906433, -0.57400910],

[0, 0.88408644]])

)

assert_allclose(

reduced_mod1.C(),

np.array([[0.59900910], [0.15394769]])

)

# Display the linear model coefficients

display(pd.DataFrame(reduced_mod1.A(), index=reduced_equation_names, columns=reduced_lead_variable_symbols))

display(pd.DataFrame(reduced_mod1.B(), index=reduced_equation_names, columns=reduced_contemporaneous_variable_symbols))

display(pd.DataFrame(reduced_mod1.C(), index=reduced_equation_names, columns=[r'$z_t$']))

| consumption | capital | |

|---|---|---|

| steady state | 0.506 | 2.65 |

| $c_{t+1}$ | $k_{t+1}$ | |

|---|---|---|

| euler equation | 1 | 0 |

| capital accumulation | 0 | 1 |

| $c_t$ | $k_t$ | |

|---|---|---|

| euler equation | 1.19 | -0.574 |

| capital accumulation | 0 | 0.884 |

| $z_t$ | |

|---|---|

| euler equation | 0.599 |

| capital accumulation | 0.154 |

Solving the model

This model can be solved using the method of Blanchard-Kahn (1980). First we put it in the required form:

\[\begin{bmatrix} \tilde k_{t+1} \\ E_t \tilde c_{t+1} \end{bmatrix} = \begin{bmatrix} B_{11} & B_{12} \\ B_{21} & B_{22} \end{bmatrix} \begin{bmatrix} \tilde k_{t} \\ \tilde c_{t} \\ \end{bmatrix} + \begin{bmatrix} C_{1} \\ C_{2} \end{bmatrix} \tilde z_t\]and the solution yields the following equilibrium dynamics:

\[\begin{bmatrix} \tilde k_{t+1} \\ \tilde c_{t+1} \end{bmatrix} = \begin{bmatrix} F_{11} & F_{12} \\ F_{21} & F_{22} \end{bmatrix} \begin{bmatrix} \tilde k_{t} \\ \tilde c_{t} \end{bmatrix} + \begin{bmatrix} G_{11} & G_{12} \\ G_{21} & G_{22} \end{bmatrix} \begin{bmatrix} \tilde z_{t+1} \\ \tilde z_t \end{bmatrix}\]in particular, we will find a policy function for the control variable, where the optimal choice for $\tilde c_t$ depends only on the contemporaneous state variable $\tilde k_t$ and exogenous shock $\tilde z_t$. Then the policy expression can be substituted in to the reduced form capital accumulation equation, providing the evolution of the state variable in terms only of itself and the exogenous shock. The evolution of the exogenous shock is an $AR(1)$ as described above.

\[\begin{align} \tilde c_t & = \phi_{ck} \tilde k_t + \phi_{cz} \tilde z_t \\ \tilde k_{t+1} & = \underbrace{\left [ F_{11} + F_{12} \phi_{ck} \right ]}_{T_{kk}} \tilde k_t + \underbrace{\left [G_{12} + F_{12} \phi_{cz} \right ]}_{T_{kz}} \tilde z_t \\ \tilde z_{t+1} & = \rho \tilde z_t + \varepsilon_t \\ \end{align}\]where $F_{11}, F_{12},$ and $G_{12}$ are defined above (and we have $G_{11} = 0$), and $\phi_{ck}, \phi_{cz}$ are generated by the solution method. $F_{21}, F_{22}, G_{21}, G_{22}$ will not be required for estimation, but can be found by forwarding the equation for $c_t$ and plugging in for $k_{t+1}$.

Some solution details

Write the Jordan decomposition of $\mathbf{B}$ as:

\[\mathbf{B} = \Lambda^{-1} J \Lambda\]where

\[\Lambda = \begin{bmatrix} \Lambda_{11} & \Lambda_{12} \\ \Lambda_{21} & \Lambda_{22} \\ \end{bmatrix} \qquad J = \begin{bmatrix} J_1 & 0 \\ 0 & J_2 \\ \end{bmatrix}\]and we assume that the eigenvalues have been re-ordered so that the explosive ones are contained in $J_2$. Note that to solve the system using the Blanchard-Kahn method, we need to separate the variables into predetermined and non-predetermined. For a unique solution to exist, it must be that the number of non-predetermined variables is equal to the number of explosive eigenvalues (so that we have “saddle-path” stability).

Here, $k_{t+1}$ is predetermined, and $c_{t+1}$ is non-predetermined, so we have a unique solution if there is one explosive eigenvalue and one non-explosive eigenvalue.

Finally we can express the coefficients in the policy function above, as (see for example DeJong and Dave, section 4.3):

\[\begin{align} \phi_{ck} & = - \Lambda_{22}^{-1} \Lambda_{21}\\ \phi_{cz} & = - \Lambda_{22}^{-1} J_2^{-1} \left (I - \rho J_2^{-1} D_2 \right )^{-1} \\ \end{align}\]where $D_2$ is the lower component of $D = \Lambda \mathbf{C}$. Here, $D_2 = \Lambda_{21} C_1 + \Lambda_{22} C_2$

def ordered_jordan_decomposition(matrix):

# Get eigenvalues and left eigenvectors of `matrix`

# Note that the left eigenvectors of `matrix`

# are the transpose of the right eigenvectors of the

# transpose of matrix, and that `matrix` and `matrix'`

# have the same eigenvalues

eigenvalues, right_eigenvectors = np.linalg.eig(matrix.transpose())

left_eigenvectors = right_eigenvectors.transpose()

# Sort in increasing order

idx = np.argsort(eigenvalues)

# Return eigenvector matrix, diagonal eigenvalue matrix

# Note that the left eigenvectors are in the rows now,

# not the columns

return np.diag(eigenvalues[idx]), left_eigenvectors[idx, :]

def solve_blanchard_kahn(B, C, rho, k_predetermined):

# Perform the Jordan decomposition

# this yields J, Lambda

eigenvalues, left_eigenvectors = ordered_jordan_decomposition(B)

left_eigenvectors = left_eigenvectors

# Dimensions

k_variables = len(B)

k_nonpredetermined = k_variables - k_predetermined

k_stable = len(np.where(eigenvalues.diagonal() < 1)[0])

k_unstable = k_variables - k_stable

# Make sure we're saddle-path stable

if not k_unstable == k_nonpredetermined:

raise RuntimeError('Blanchard-Kahn condition not met. Unique solution does not exist')

# Decouple the system (this is D, above)

decoupled_C = np.dot(left_eigenvectors, C)

# Create partition indices

p1 = np.s_[:k_predetermined]

p2 = np.s_[k_predetermined:]

p11 = np.s_[:k_predetermined, :k_predetermined]

p12 = np.s_[:k_predetermined, k_predetermined:]

p21 = np.s_[k_predetermined:, :k_predetermined]

p22 = np.s_[k_predetermined:, k_predetermined:]

# Solve the explosive component (controls) in terms of the

# non-explosive component (states) and shocks

tmp = np.linalg.inv(left_eigenvectors[p22])

# This is \phi_{ck}, above

policy_state = - np.dot(tmp, left_eigenvectors[p21])

# This is \phi_{cz}, above

policy_shock = -(

np.dot(tmp, 1. / eigenvalues[p22]).dot(

np.linalg.inv(

np.eye(k_nonpredetermined) -

rho / eigenvalues[p22]

)

).dot(decoupled_C[p2])

)

# Solve for the non-explosive transition

# This is T_{kk}, above

transition_state = B[p11] + np.dot(B[p12], policy_state)

# This is T_{kz}, above

transition_shock = np.dot(B[p12], policy_shock) + C[p1]

return policy_state, policy_shock, transition_state, transition_shock

class ReducedRBC2(ReducedRBC1):

def solve(self, params=None):

# Update the model parameters, if given

if params is not None:

self.update(params)

# Solve the model

phi_ck, phi_cz, T_kk, T_kz = solve_blanchard_kahn(

self.B(), self.C(),

self.technology_shock_persistence, 1

)

# Create the design matrix

inv_capital_share = 1. / self.capital_share

tmp1 = (1 - self.capital_share) * inv_capital_share

phi_yk = 1 - tmp1 * phi_ck

phi_yz = inv_capital_share - tmp1 * phi_cz

phi_nk = 1 - inv_capital_share * phi_ck

phi_nz = inv_capital_share * (1 - phi_cz)

design = np.r_[

phi_yk, phi_yz, phi_nk, phi_nz, phi_ck, phi_cz

].reshape((3,2))

# Create the transition matrix

transition = np.r_[

T_kk[0,0], T_kz[0,0], 0, self.technology_shock_persistence

].reshape((2,2))

return design, transition

reduced_mod2 = ReducedRBC2(parameters['value'])

# Check the Blanchard-Kahn conditions

eigenvalues, left_eigenvectors = ordered_jordan_decomposition(reduced_mod2.B())

print('Modulus of eigenvalues of B:', np.abs(eigenvalues.diagonal()))

# Test the eigenvalues and eigenvectors

# (results from "Emsm", downloaded from

# https://sites.google.com/site/frugemurcia/home/replication-files

# on 06/19/2015)

assert_allclose(eigenvalues.diagonal(), [0.88408644, 1.1906433])

assert_allclose(left_eigenvectors[0,:], [0, 1])

# Note the second eigenvector returned by numpy

# is scaled differently than the one returned

# by Gauss, so we need to rescale it to compare.

assert_allclose(

left_eigenvectors[1,:] / left_eigenvectors[1,1],

[-0.53406267, 1]

)

# Solve the model

design, transition = reduced_mod2.solve()

# Test the solved model coefficients for accuracy

assert_allclose(design[2,:], [0.53406267, 0.48719795])

# Display the results

display(pd.DataFrame(

np.r_[design[2,:], transition[0,:]],

columns=['solution'],

index=[r'$\phi_{ck}$', r'$\phi_{cz}$', r'$T_{kk}$', r'$T_{kz}$']

).T)

Modulus of eigenvalues of B: [0.884 1.191]

| $\phi_{ck}$ | $\phi_{cz}$ | $T_{kk}$ | $T_{kz}$ | |

|---|---|---|---|---|

| solution | 0.534 | 0.487 | 0.884 | 0.319 |

State-space form

Assuming that $\xi_t = (\tilde k_t, \tilde z_t)’$ is unobservable and $s_t = (\tilde y_t, \tilde n_t, \tilde c_t)’$ is observable, the above equations give use the following relationship:

\[\begin{align} \begin{bmatrix} \tilde y_t \\ \tilde n_t \\ \tilde c_t \\ \end{bmatrix} & = \begin{bmatrix} \phi_{yk} & \phi_{yz} \\ \phi_{nk} & \phi_{nz} \\ \phi_{ck} & \phi_{cz} \\ \end{bmatrix} \begin{bmatrix} \tilde k_{t} \\ \tilde z_{t} \end{bmatrix} \\ & = \begin{bmatrix} 1 - \frac{1-\alpha}{\alpha} \phi_{ck} & \frac{1}{\alpha} - \frac{1-\alpha}{\alpha} \phi_{cz} \\ 1 - \frac{1}{\alpha} \phi_{ck} & \frac{1}{\alpha} \left [ 1 - \phi_{cz} \right ] \\ \phi_{ck} & \phi_{cz} \\ \end{bmatrix} \begin{bmatrix} \tilde k_{t} \\ \tilde z_{t} \end{bmatrix} \end{align}\]The above is the observation equation. In order to overcome the stochastic singularity problem, we augment with measurement errors $u_t = (u_{yt}, u_{nt}, u_{ct})’$:

\[\begin{align} s_t & = \mathbf{\Phi} \xi_t + u_t \end{align}\]And the transition equation is:

\[\begin{align} \begin{bmatrix} \tilde k_{t+1} \\ \tilde z_{t+1} \\ \end{bmatrix} & = \begin{bmatrix} T_{kk} & T_{kz}\\ 0 & \rho \\ \end{bmatrix} \begin{bmatrix} \tilde k_{t} \\ \tilde z_{t} \end{bmatrix} + \begin{bmatrix} 0 \\ 1 \end{bmatrix} \varepsilon_t \end{align}\]The Python package statsmodels has support for maximum likelihood analysis of state space models.

Calibration

There are six parameters

\[\{ \beta, \psi, \delta, \alpha, \rho, \sigma^2 \}\]and of those three will be calibrated: ${ \psi = 3, \delta = 0.025, \alpha = 0.36 }$ (note that $\psi$ only influences the steady-state labor supply and so does not enter into the state-space form parameters). The calibration is done because the model has difficulty estimating all of the parameters, see Ruge-Murcia (2007) for more details.

The remaining three parameters, ${ \beta, \rho, \sigma^2 }$, will be estimated by maximum likelhood.

Data

We will evaluate the model using two datasets. The first will be simulated, allowing us to explore the capacity of the model to recover the true parameters. The second will estimate the model on observed economic data.

Simulated dataset

As in Ruge-Murcia (2007), we can simulate the linear model.

np.random.seed(12345)

# Parameters

T = 200 # number of periods to simulate

T0 = 100 # number of initial periods to "burn"

# We can use the exact random draws from "Emsm", downloaded from

# https://sites.google.com/site/frugemurcia/home/replication-files

# on 06/19/2015)

rm2007_eps = [0.0089954547, 0.069601997, -0.0081704445, -0.036704078, -0.026966673, -0.013741121, 0.0089339760, -0.0056557030, -0.0073353523, 0.027214134, 0.0036223219, -0.033331014, 0.032539993, 0.044695276, 0.012599442, -0.020012497, -0.065070833, 0.024777248, -0.058297234, -0.072139533, 0.080062379, 0.023164655, -0.028318809, 0.023734384, -0.023575740, 0.058697373, -0.00080918191, 0.029482310, 0.059178715, -0.010752551, 0.049127695, 0.063137227, -0.015733529, 0.018006224, 0.051256459, -0.014467873, 0.042611930, -0.078176552, -0.0040812905, -0.0086694118, 0.016261678, 0.0055330257, 0.026286130, -0.0066732973, 0.019133914, 0.018442169, 0.0046151171, 0.0015229921, 0.047776839, -0.058401266, 0.014895019, -0.0070732464, -0.036637349, 0.018778403, 0.0030934044, -0.033385312, -0.0044036385, -0.0029289904, -0.029415234, -0.010308393, -0.023496361, -0.023784028, 0.045396730, -0.021532569, -0.086991302, 0.046579589, 0.015086674, 0.0054060766, 0.0094114004, 0.014372645, -0.060998265, -0.0047493261, -0.030991307, -0.022061370, -0.020225482, -0.013470628, -0.013967446, -0.021552474, -0.054801903, -0.0052111107, 0.0080784668, 0.042868645, -0.0015220824, -0.061354829, 0.053529145, -0.020002403, -0.00053686088, 0.085988265, 0.037919020, 0.023531373, 0.0046336046, 0.012880821, 0.0037651140, -0.059647623, -0.027420909, -0.063257854, -0.010324261, -0.025627797, -0.017646345, -0.00091871809, 0.0066086013, 0.0018793222, 0.019543168, -0.031823750, -0.0092249652, 0.013246704, 0.014181125, 0.047271352, 0.047259268, 0.010107337, -0.083925083, -0.036031657, -0.0022387325, -0.035090684, -0.022218572, -0.017554625, 0.033953597, 0.010744674, -0.010891498, -0.0035293110, -0.033522281, -0.072168448, -0.0042416089, -0.025190520, 0.11066349, 0.029308577, -0.018047271, 0.055748729, -0.0016904632, -0.035578602, -0.10830804, -0.013671301, -0.010389470, -0.012295055, 0.055696357, 0.020597878, 0.026447061, -0.054887926, -0.045563156, 0.060229793, 0.028380999, -0.0034341303, 0.038103203, 0.012224323, 0.016752740, -0.0065436404, -0.0010711498, -0.025486203, -0.055621838, 0.0096008728, -0.088779172, 0.092452909, 0.057714587, -0.0057425132, 0.023627700, -0.029821882, -0.012037717, -0.074682148, -0.062682990, -0.038800349, -0.094946077, 0.074545642, -0.00050272713, -0.0075839744, -0.037362343, 0.012332294, 0.10490393, 0.049997520, 0.033916235, -0.061734224, -0.015363425, 0.057711167, -0.051687840, 0.031219589, 0.041031894, 0.0051038726, -0.013144180, 0.054156433, -0.0090438895, 0.023331707, -0.0079434321, -0.0029084658, -0.0064262300, 0.044577448, 0.014816901, 0.043276307, -0.011412684, -0.0026201902, -0.021138420, -0.0020795206, -0.042017897, -0.028148295, 0.063945871, -0.049724502, -0.048571001, -0.061207381, 0.050007129, 0.0062884061, 0.057948665, -0.012780170, -0.020464058, 0.023577863, 0.030007840, -0.013682281, 0.044281158, 0.033864209, -0.016235593, 0.0052712906, 0.035426922, -0.084935662, -0.061241657, 0.038759520, 0.019838792, -0.038971482, -0.043112193, -0.10098203, 0.011744644, 0.014708720, 0.035224935, 0.0098378679, 0.031205446, 0.026015597, -0.048897576, -0.042539822, -0.036330332, -0.033689415, 0.029665808, 0.0086127051, 0.038663112, -0.064534479, -0.036174560, -0.034225451, -0.0084848888, -0.011724560, -0.037544322, -0.013054490, -0.062983798, 0.011448707, 0.0022791918, -0.054508196, 0.046134801, -0.063884585, 0.048918326, 0.018358644, -0.011278321, 0.021175611, -0.0069196463, -0.084987826, 0.016286265, -0.031783692, -0.041129528, -0.11686860, 0.0040626993, 0.057649830, 0.019174675, -0.010319778, 0.080549326, -0.058124228, -0.027757539, -0.0028474062, 0.012399938, -0.088780901, 0.077048657, 0.070548177, -0.023784957, 0.035935388, 0.064960358, 0.019987594, 0.062245578, 0.0014217956, 0.057173164, 0.043800495, -0.023484057, 0.021398628, -0.012723988, 0.012587101, -0.049855702, 0.070557277, -0.017640273, -0.031555592, -0.030900124, -0.028508626, -0.029129143, 0.0024196883, -0.026937200, -0.011642554, -0.045071194, -0.013049519, -0.021908382, 0.017900266, -0.019798107, -0.040774046, -0.027013698, 0.065691125, 0.0081570086, -0.012601818, 0.017918061, 0.017225503, 0.0021227212, 0.032141622, 0]

# Or we can draw our own

gen_eps = np.random.normal(0, reduced_mod1.technology_shock_std, size=(T+T0+1))

eps = rm2007_eps

# Create and solve the model

reduced_mod2 = ReducedRBC2(parameters['value'])

design, transition = reduced_mod2.solve()

selection = np.array([0, 1])

# Generate variables

raw_observed = np.zeros((T+T0+1,3))

raw_state = np.zeros((T+T0+2,2))

for t in range(T+T0+1):

raw_observed[t] = np.dot(design, raw_state[t])

raw_state[t+1] = np.dot(transition, raw_state[t]) + selection * eps[t]

# Test that our simulated series are the same as in "Emsm"

# Note: Gauss uses ddof=1 for std dev calculation

assert_allclose(np.mean(raw_state[1:-1,:], axis=0), [-0.0348286036, -0.0133121934])

assert_allclose(np.std(raw_state[1:-1,:], axis=0, ddof=1), [0.122766006, 0.0742206044])

assert_allclose(np.mean(raw_observed[1:,:], axis=0), [-0.027208998, -0.0021226675, -0.025086330])

assert_allclose(np.std(raw_observed[1:,:], axis=0, ddof=1), [0.14527028, 0.089694148, 0.090115364])

# Drop the first 100 observations

sim_observed = raw_observed[T0+1:,:]

sim_state = raw_state[T0+1:-1,:]

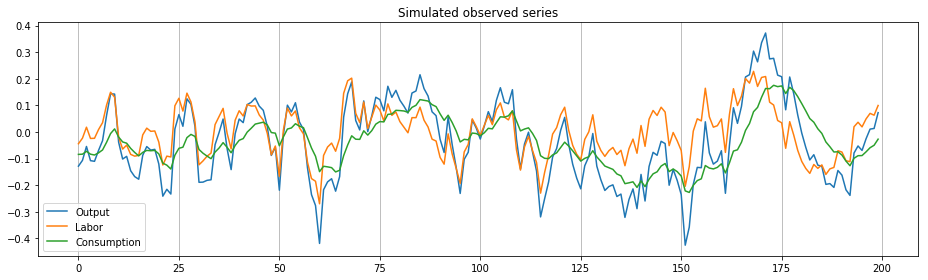

fig, ax = plt.subplots(figsize=(13,4))

ax.plot(sim_observed[:,0], label='Output')

ax.plot(sim_observed[:,1], label='Labor')

ax.plot(sim_observed[:,2], label='Consumption')

ax.set_title('Simulated observed series')

ax.xaxis.grid()

ax.legend(loc='lower left')

fig.tight_layout();

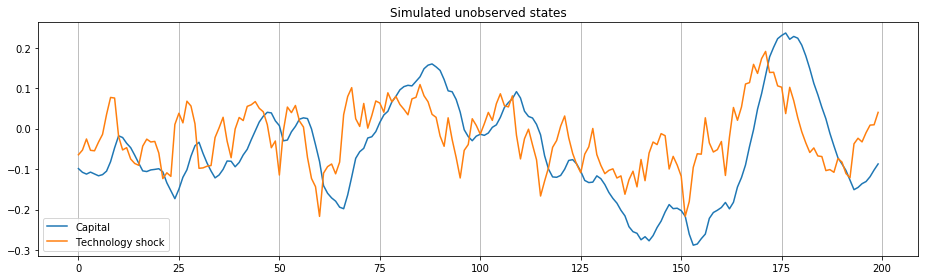

fig, ax = plt.subplots(figsize=(13,4))

ax.plot(sim_state[:,0], label='Capital')

ax.plot(sim_state[:,1], label='Technology shock')

ax.set_title('Simulated unobserved states')

ax.xaxis.grid()

ax.legend(loc='lower left')

fig.tight_layout();

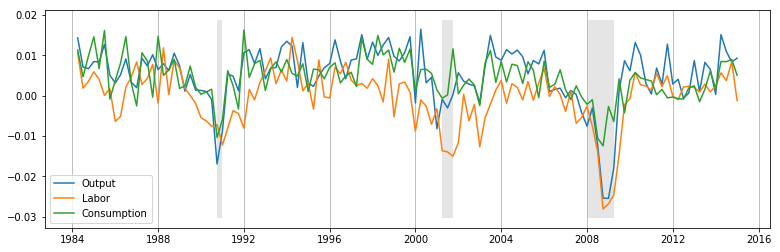

Observed economic data

We use data on hours worked, consumption, and investment

# Get some data

start='1984-01'

end = '2015-01'

labor = DataReader('HOANBS', 'fred', start=start, end=end) # hours

consumption = DataReader('PCECC96', 'fred', start=start, end=end) # billions of dollars

investment = DataReader('GPDI', 'fred', start=start, end=end) # billions of dollars

population = DataReader('CNP16OV', 'fred', start=start, end=end) # thousands of persons

recessions = DataReader('USRECQ', 'fred', start=start, end=end)

# Collect the raw values

raw = pd.concat((labor, consumption, investment, population.resample('QS').mean()), axis=1)

raw.columns = ['labor', 'consumption', 'investment', 'population']

raw['output'] = raw['consumption'] + raw['investment']

# Make the data consistent with the model

y = np.log(raw.output * 10**(9-3) / raw.population)

n = np.log(raw.labor * (1e3 * 40) / raw.population)

c = np.log(raw.consumption * 10**(9-3) / raw.population)

# Make the data stationary

y = y.diff()[1:]

n = n.diff()[1:]

c = c.diff()[1:]

# Construct the final dataset

econ_observed = pd.concat((y, n, c), axis=1)

econ_observed.columns = ['output','labor','consumption']

fig, ax = plt.subplots(figsize=(13,4))

dates = econ_observed.index._mpl_repr()

ax.plot(dates, econ_observed.output, label='Output')

ax.plot(dates, econ_observed.labor, label='Labor')

ax.plot(dates, econ_observed.consumption, label='Consumption')

rec = recessions.resample('QS').last().loc[econ_observed.index[0]:].iloc[:, 0].values

ylim = ax.get_ylim()

ax.fill_between(dates, ylim[0]+1e-5, ylim[1]-1e-5, rec, facecolor='k', alpha=0.1)

ax.xaxis.grid()

ax.legend(loc='lower left');

Estimation

class EstimateRBC1(sm.tsa.statespace.MLEModel):

def __init__(self, output=None, labor=None, consumption=None,

measurement_errors=True,

disutility_labor=3, depreciation_rate=0.025,

capital_share=0.36, **kwargs):

# Determine provided observed variables

self.output = output is not None

self.labor = labor is not None

self.consumption = consumption is not None

self.observed_mask = (

np.array([self.output, self.labor, self.consumption], dtype=bool)

)

observed_variables = np.r_[['output', 'labor', 'consumption']]

self.observed_variables = observed_variables[self.observed_mask]

self.measurement_errors = measurement_errors

# Construct the full endogenous array

endog = []

if self.output:

endog.append(np.array(output))

if self.labor:

endog.append(np.array(labor))

if self.consumption:

endog.append(np.array(consumption))

endog = np.c_[endog].transpose()

# Initialize the statespace model

super(EstimateRBC1, self).__init__(endog, k_states=2, k_posdef=1, **kwargs)

self.initialize_stationary()

self.data.ynames = self.observed_variables

# Check for stochastic singularity

if self.k_endog > 1 and not measurement_errors:

raise ValueError('Stochastic singularity encountered')

# Save the calibrated parameters

self.disutility_labor = disutility_labor

self.depreciation_rate = depreciation_rate

self.capital_share = capital_share

# Create the structural model

self.structural = ReducedRBC2()

# Setup fixed elements of the statespace matrices

self['selection', 1, 0] = 1

idx = np.diag_indices(self.k_endog)

self._idx_obs_cov = ('obs_cov', idx[0], idx[1])

@property

def start_params(self):

start_params = [0.99, 0.5, 0.01]

if self.measurement_errors:

start_meas_error = np.r_[[0.1]*3]

start_params += start_meas_error[self.observed_mask].tolist()

return start_params

@property

def param_names(self):

param_names = ['beta', 'rho', 'sigma.vareps']

if self.measurement_errors:

meas_error_names = np.r_[['sigma2.y', 'sigma2.n', 'sigma2.c']]

param_names += meas_error_names[self.observed_mask].tolist()

return param_names

def transform_params(self, unconstrained):

constrained = np.zeros(unconstrained.shape, unconstrained.dtype)

# Discount rate is between 0 and 1

constrained[0] = max(1 / (1 + np.exp(unconstrained[0])) - 1e-4, 1e-4)

# Technology shock persistence is between -1 and 1

constrained[1] = unconstrained[1] / (1 + np.abs(unconstrained[1]))

# Technology shock std. dev. is positive

constrained[2] = np.abs(unconstrained[2])

# Measurement error variances must be positive

if self.measurement_errors:

constrained[3:3+self.k_endog] = unconstrained[3:3+self.k_endog]**2

return constrained

def untransform_params(self, constrained):

unconstrained = np.zeros(constrained.shape, constrained.dtype)

# Discount rate is between 0 and 1

unconstrained[0] = np.log((1 - constrained[0] + 1e-4) / (constrained[0] + 1e-4))

# Technology shock persistence is between -1 and 1

unconstrained[1] = constrained[1] / (1 + constrained[1])

# Technology shock std. dev. is positive

unconstrained[2] = constrained[2]

# Measurement error variances must be positive

if self.measurement_errors:

unconstrained[3:3+self.k_endog] = constrained[3:3+self.k_endog]**0.5

return unconstrained

def update(self, params, **kwargs):

params = super(EstimateRBC1, self).update(params, **kwargs)

# Get the parameters of the structural model

# Note: we are calibrating three parameters

structural_params = np.r_[

params[0],

self.disutility_labor,

self.depreciation_rate,

self.capital_share,

params[1:3]

]

# Solve the model

design, transition = self.structural.solve(structural_params)

# Update the statespace representation

self['design'] = design[self.observed_mask, :]

if self.measurement_errors:

self[self._idx_obs_cov] = params[3:3+self.k_endog]

self['transition'] = transition

self['state_cov', 0, 0] = self.structural.technology_shock_std**2

Estimation on simulated data

# Setup the statespace model

sim_mod = EstimateRBC1(

output=sim_observed[:,0],

labor=sim_observed[:,1],

consumption=sim_observed[:,2],

measurement_errors=True

)

# sim_res = sim_mod.fit(maxiter=1000, information_matrix_type='oim')

sim_res = sim_mod.fit(maxiter=1000)

print(sim_res.summary())

/Users/fulton/miniconda3/envs/python3/lib/python3.6/site-packages/ipykernel_launcher.py:75: RuntimeWarning: overflow encountered in exp

Statespace Model Results

============================================================================================

Dep. Variable: ['output' 'labor' 'consumption'] No. Observations: 200

Model: EstimateRBC1 Log Likelihood 3160.668

Date: Thu, 01 Nov 2018 AIC -6309.336

Time: 20:36:40 BIC -6289.546

Sample: 0 HQIC -6301.328

- 200

Covariance Type: opg

================================================================================

coef std err z P>|z| [0.025 0.975]

--------------------------------------------------------------------------------

beta 0.9500 5.57e-06 1.7e+05 0.000 0.950 0.950

rho 0.8499 8.3e-05 1.02e+04 0.000 0.850 0.850

sigma.vareps 0.0440 1.23e-06 3.58e+04 0.000 0.044 0.044

sigma2.y 5.362e-10 5.39e-09 0.099 0.921 -1e-08 1.11e-08

sigma2.n 4.172e-05 8.27e-05 0.504 0.614 -0.000 0.000

sigma2.c 8.71e-13 4.81e-09 0.000 1.000 -9.43e-09 9.43e-09

======================================================================================

Ljung-Box (Q): 40.66, 0.21, 79.19 Jarque-Bera (JB): 0.09, 318540.26, 0.08

Prob(Q): 0.44, 1.00, 0.00 Prob(JB): 0.95, 0.00, 0.96

Heteroskedasticity (H): 0.86, 0.00, 0.66 Skew: -0.05, 13.96, 0.04

Prob(H) (two-sided): 0.54, 0.00, 0.09 Kurtosis: 2.95, 196.51, 2.93

======================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

[2] Covariance matrix is singular or near-singular, with condition number 5.64e+18. Standard errors may be unstable.

/Users/fulton/projects/statsmodels/statsmodels/base/model.py:508: ConvergenceWarning: Maximum Likelihood optimization failed to converge. Check mle_retvals

"Check mle_retvals", ConvergenceWarning)

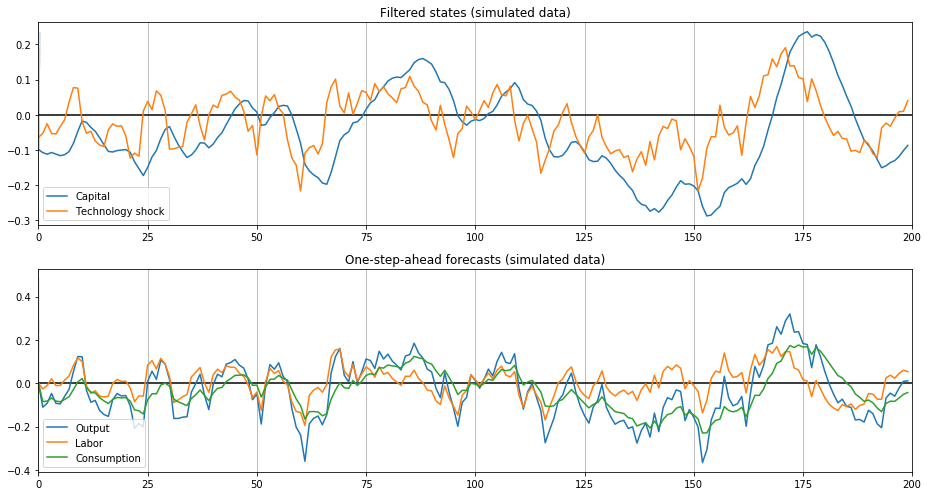

fig, axes = plt.subplots(2, 1, figsize=(13,7))

# Filtered states confidence intervals

states_cov = np.diagonal(sim_res.filtered_state_cov).T

states_upper = sim_res.filtered_state + 1.96 * states_cov**0.5

states_lower = sim_res.filtered_state - 1.96 * states_cov**0.5

ax = axes[0]

lines, = ax.plot(sim_res.filtered_state[0], label='Capital')

ax.fill_between(states_lower[0], states_upper[0], color=lines.get_color(), alpha=0.2)

lines, = ax.plot(sim_res.filtered_state[1], label='Technology shock')

ax.fill_between(states_lower[1], states_upper[1], color=lines.get_color(), alpha=0.2)

ax.set_xlim((0, 200))

ax.hlines(0, 0, 200)

ax.set_title('Filtered states (simulated data)')

ax.legend(loc='lower left')

ax.xaxis.grid()

ax = axes[1]

# One-step-ahead forecasts confidence intervals

forecasts_cov = np.diagonal(sim_res.forecasts_error_cov).T

forecasts_upper = sim_res.forecasts + 1.96 * forecasts_cov**0.5

forecasts_lower = sim_res.forecasts - 1.96 * forecasts_cov**0.5

for i in range(sim_mod.k_endog):

lines, = ax.plot(sim_res.forecasts[i], label=sim_mod.endog_names[i].title())

ax.fill_between(forecasts_lower[i], forecasts_upper[i], color=lines.get_color(), alpha=0.1)

ax.set_xlim((0, 200))

ax.hlines(0, 0, 200)

ax.set_title('One-step-ahead forecasts (simulated data)')

ax.legend(loc='lower left')

ax.xaxis.grid()

fig.tight_layout();

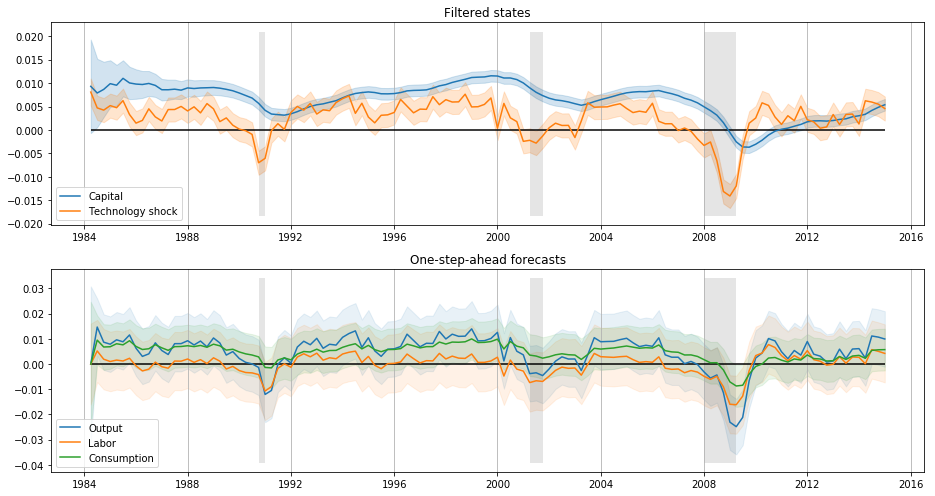

Estimation on observed data

# Setup the statespace model

econ_mod = EstimateRBC1(

output=econ_observed['output'],

labor=econ_observed['labor'],

consumption=econ_observed['consumption'],

measurement_errors=True,

dates=econ_observed.index

)

econ_res = econ_mod.fit(maxiter=1000, information_matrix_type='oim')

print(econ_res.summary())

Statespace Model Results

============================================================================================

Dep. Variable: ['output' 'labor' 'consumption'] No. Observations: 124

Model: EstimateRBC1 Log Likelihood 1446.774

Date: Thu, 01 Nov 2018 AIC -2881.547

Time: 20:36:43 BIC -2864.625

Sample: 04-01-1984 HQIC -2874.673

- 01-01-2015

Covariance Type: opg

================================================================================

coef std err z P>|z| [0.025 0.975]

--------------------------------------------------------------------------------

beta 0.9850 0.010 96.667 0.000 0.965 1.005

rho 0.9616 0.023 42.722 0.000 0.918 1.006

sigma.vareps 0.0022 0.000 9.797 0.000 0.002 0.003

sigma2.y 9.75e-06 2.58e-06 3.775 0.000 4.69e-06 1.48e-05

sigma2.n 2.398e-05 4.66e-06 5.143 0.000 1.48e-05 3.31e-05

sigma2.c 1.568e-05 2.16e-06 7.251 0.000 1.14e-05 1.99e-05

=====================================================================================

Ljung-Box (Q): 38.83, 120.95, 47.83 Jarque-Bera (JB): 16.90, 0.23, 3.25

Prob(Q): 0.52, 0.00, 0.18 Prob(JB): 0.00, 0.89, 0.20

Heteroskedasticity (H): 1.68, 0.90, 0.53 Skew: 0.40, -0.11, 0.32

Prob(H) (two-sided): 0.10, 0.74, 0.05 Kurtosis: 4.62, 3.01, 3.46

=====================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

fig, axes = plt.subplots(2, 1, figsize=(13,7))

# Filtered states confidence intervals

states_cov = np.diagonal(econ_res.filtered_state_cov).T

states_upper = econ_res.filtered_state + 1.96 * states_cov**0.5

states_lower = econ_res.filtered_state - 1.96 * states_cov**0.5

ax = axes[0]

lines, = ax.plot(dates, econ_res.filtered_state[0], label='Capital')

ax.fill_between(dates, states_lower[0], states_upper[0], color=lines.get_color(), alpha=0.2)

lines, = ax.plot(dates, econ_res.filtered_state[1], label='Technology shock')

ax.fill_between(dates, states_lower[1], states_upper[1], color=lines.get_color(), alpha=0.2)

ylim = ax.get_ylim()

ax.fill_between(dates, ylim[0]+1e-4, ylim[1]-1e-4, rec, facecolor='k', alpha=0.1)

ax.hlines(0, dates[0], dates[-1])

ax.set_title('Filtered states')

ax.legend(loc='lower left')

ax.xaxis.grid()

ax = axes[1]

# One-step-ahead forecasts confidence intervals

forecasts_cov = np.diagonal(econ_res.forecasts_error_cov).T

forecasts_upper = econ_res.forecasts + 1.96 * forecasts_cov**0.5

forecasts_lower = econ_res.forecasts - 1.96 * forecasts_cov**0.5

for i in range(econ_mod.k_endog):

lines, = ax.plot(dates, econ_res.forecasts[i], label=econ_mod.endog_names[i].title())

ax.fill_between(dates, forecasts_lower[i], forecasts_upper[i], color=lines.get_color(), alpha=0.1)

ylim = ax.get_ylim()

ax.fill_between(dates, ylim[0]+1e-4, ylim[1]-1e-4, rec, facecolor='k', alpha=0.1)

ax.hlines(0, dates[0], dates[-1])

ax.set_title('One-step-ahead forecasts')

ax.legend(loc='lower left')

ax.xaxis.grid()

fig.tight_layout();

References

[1] DeJong, David N., and Chetan Dave. 2011.

Structural Macroeconometrics. Second edition.

Princeton: Princeton University Press.

[2] Ruge-Murcia, Francisco J. 2007.

"Methods to Estimate Dynamic Stochastic General Equilibrium Models."

Journal of Economic Dynamics and Control 31 (8): 2599–2636.