State space diagnostics(Open on Google Colab | View / download notebook | Report a problem)

Table of Contents

State space diagnostics

It is important to run post-estimation diagnostics on all types of models. In state space models, if the model is correctly specified, the standardized one-step ahead forecast errors should be independent and identically Normally distributed. Thus, one way to assess whether or not the model adequately describes the data is to compute the standardized residuals and apply diagnostic tests to check that they meet these distributional assumptions.

Although there are many available tests, Durbin and Koopman (2012) and Harvey (1990) suggest three basic tests as a starting point:

- Normality: the Jarque–Bera test

- Heterskedasticity: a test similar to the Goldfeld-Quandt test

- Serial correlation: the Ljung-Box test

These have been added to Statsmodels in this pull request (2431), and their results are added as an additional table at the bottom of the summary output (see the table below for an example).

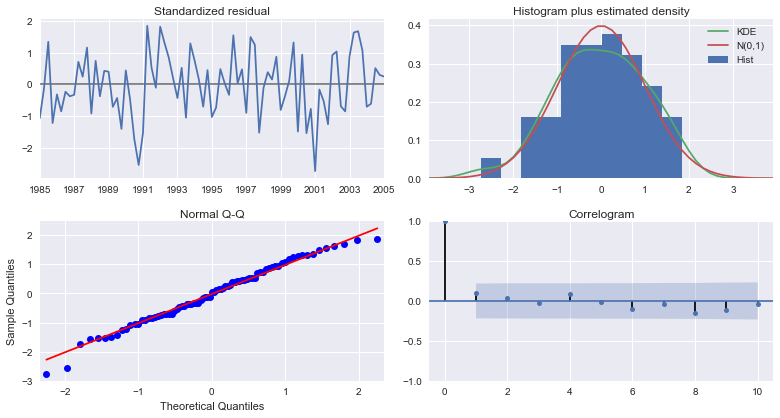

Furthermore, graphical tools can be useful in assessing these assumptions. Durbin and Koopman (2012) suggest the following four plots as a starting point:

- A time-series plot of the standardized residuals themselves

- A histogram and kernel-density of the standardized residuals, with a reference plot of the Normal(0,1) density

- A Q-Q plot against Normal quantiles

- A correlogram

To that end, I have also added a plot_diagnostics method which creates those following four plots.

%matplotlib inline

import numpy as np

import statsmodels.api as sm

import seaborn as sn

from pandas_datareader.data import DataReader

lgdp = np.log(DataReader('GDPC1', 'fred', start='1984-01', end='2005-01'))

mod = sm.tsa.SARIMAX(lgdp, order=(2,1,0), seasonal_order=(3,1,0,3))

res = mod.fit()

print res.summary()

fig = res.plot_diagnostics(figsize=(11,6))

fig.tight_layout()

Statespace Model Results

=========================================================================================

Dep. Variable: GDPC1 No. Observations: 85

Model: SARIMAX(2, 1, 0)x(3, 1, 0, 3) Log Likelihood 310.194

Date: Sun, 22 Jan 2017 AIC -608.389

Time: 14:23:06 BIC -593.733

Sample: 01-01-1984 HQIC -602.494

- 01-01-2005

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

ar.L1 0.1672 0.111 1.507 0.132 -0.050 0.385

ar.L2 0.3217 0.115 2.808 0.005 0.097 0.546

ar.S.L3 -0.8389 0.128 -6.551 0.000 -1.090 -0.588

ar.S.L6 -0.4778 0.186 -2.564 0.010 -0.843 -0.112

ar.S.L9 -0.0558 0.120 -0.463 0.643 -0.292 0.180

sigma2 2.681e-05 5.16e-06 5.193 0.000 1.67e-05 3.69e-05

===================================================================================

Ljung-Box (Q): 32.74 Jarque-Bera (JB): 1.05

Prob(Q): 0.79 Prob(JB): 0.59

Heteroskedasticity (H): 1.09 Skew: -0.23

Prob(H) (two-sided): 0.82 Kurtosis: 2.70

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).